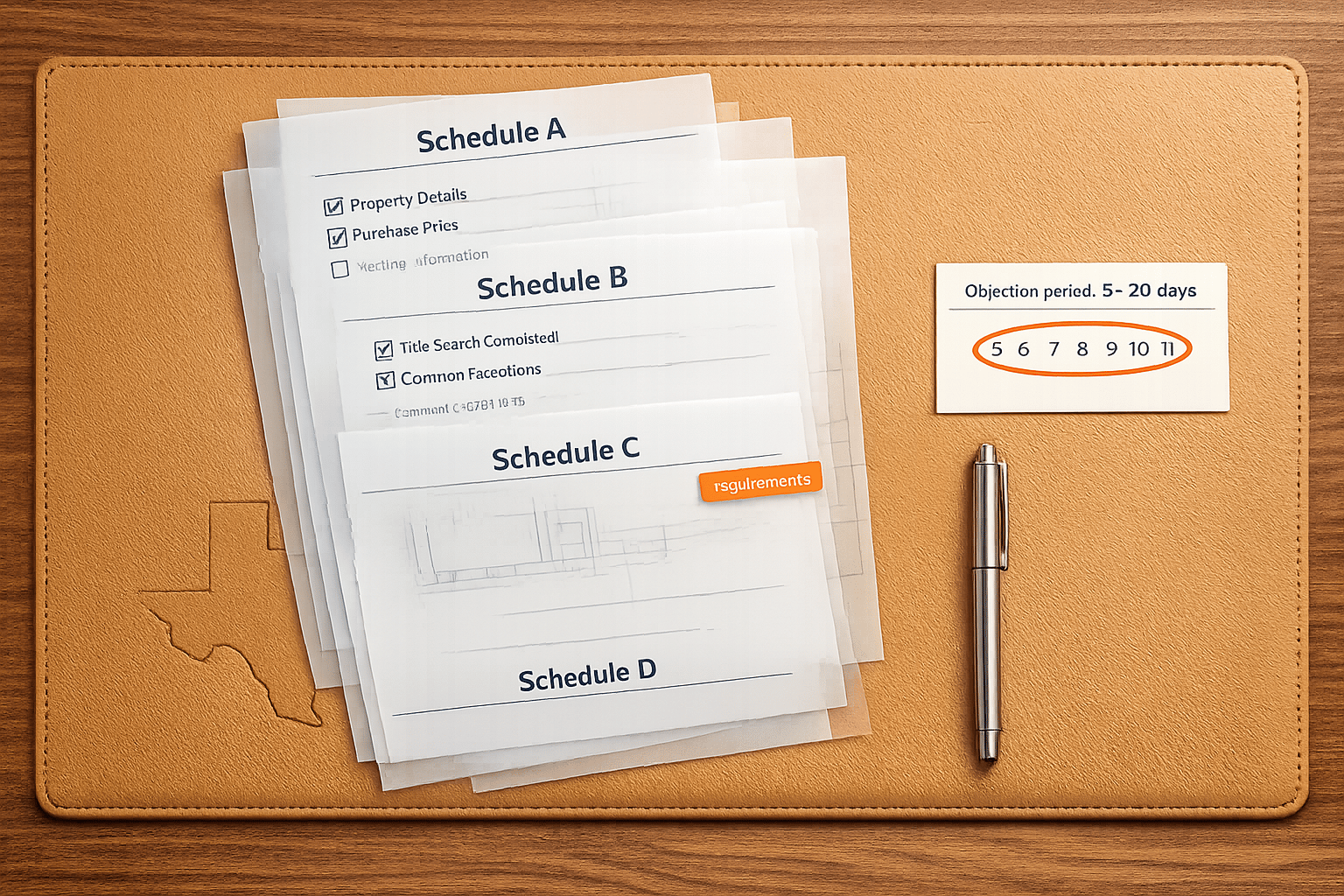

A Texas title commitment is a key document in commercial real estate (CRE) transactions. It outlines what the title insurance will cover, identifies risks, and lists conditions to finalize the policy. In Texas, title commitments follow a standardized four-schedule format (A, B, C, D) regulated by the Texas Department of Insurance. This ensures transparency and consistency but requires careful review due to unique factors like mineral rights and community property laws.

Key points for buyers, lenders, and advisors:

- Schedule A: Verify transaction details (buyer, seller, legal description, coverage amounts).

- Schedule B: Understand exceptions (easements, mineral rights, CC&Rs) and assess their impact.

- Schedule C: Fulfill all requirements (lien releases, tax payments, corporate documents) to close.

- Schedule D: Review ownership and premium breakdown for the title company.

Act fast – Texas contracts typically allow 5 to 20 days to raise objections. Missing this window means accepting all exceptions and restrictions, which could lead to costly issues later. Use a tracking system to manage deadlines and ensure a smooth closing process.

Texas Title Commitment: 4-Schedule Breakdown for CRE Deals

Pre-Commitment Preparation

Gather Key Transaction Details

Before reaching out to a title company, double-check the roles and exact legal names of all parties involved, as recorded in Texas public records. Attorney David J. Willis emphasizes the importance of this step:

"Capacity is as important as identity. Title companies want the correct person executing closing documents in the capacity in which that person is acting." [4]

It’s crucial to confirm the specific capacity in which each party is acting – whether as an individual, an LLC manager, a trustee, a general partner, or an executor. For entities like LLCs or corporations, ensure their names match exactly with Texas Secretary of State filings. Even a small mismatch can lead to delays and the need for correction instruments, which can cost both time and money.

Additionally, address two Texas-specific concerns: marital status and mineral rights. Texas is one of nine community property states in the U.S., which means a seller’s spouse might need to sign at closing, even if their name isn’t on the deed [5]. Also, verify whether the surface and mineral estates have been severed, as the mineral estate is the dominant estate in Texas and could significantly impact development plans [5].

Documents to Have Before Ordering Title

Getting the right documents together before placing a title order can streamline the process and minimize back-and-forth with the title company. At the core is the executed Purchase and Sale Agreement (PSA) – this document opens escrow and sets the transaction framework [1][2]. Pair this with a detailed legal description of the property (such as metes and bounds or lot and block), which defines the area being searched [1][2].

For commercial real estate (CRE) transactions, include all relevant entity documents. These might include Certificates of Formation, Operating Agreements, Bylaws, and Corporate Resolutions, which confirm who has the authority to sign on behalf of the buyer or seller [6][7]. Attorney Afton Baily Griffin from Amaral Tellawi Law explains:

"Deciding how a property will be held (outright, in a business entity like an LLC, in a trust, or some combination of these) is often referred to as the ‘asset protection’ strategy and should be done as early as possible." [7]

If the entity that will hold the property hasn’t been formed yet, include "and/or its assigns" in the buyer’s name on the contract. This allows for a smooth transfer later without needing lender approval or contract amendments [7]. Also, gather any prior title policies and existing surveys, as these can help the title company work faster and identify any long-standing exceptions early in the process [6][2].

With these documents in hand, you’ll be ready to move on to the next step: setting up systems to track and manage title exceptions.

Set Up Review and Tracking Systems

Once you’ve secured the key documents, it’s time to prepare for the review process. The title company will issue a Guaranty File (GF) number, which serves as the central reference point for all documents, communications, and requirements tied to the transaction [4]. Make sure your team uses this number consistently.

The clock for raising title objections starts as soon as the title commitment is issued. Under Texas contracts, buyers typically have 5 to 20 days to submit objections [2]. Missing this window means all listed exceptions are automatically accepted. To stay on top of this, create a tracking matrix before the commitment arrives. Include columns for each item, its impact on the deal, the required action, the responsible party, and the deadline.

| Tracking Column | Purpose |

|---|---|

| Item/Exception | Specific Schedule B or C item number and description |

| Impact | How it affects the property (e.g., "Blocks planned expansion") |

| Solution | Action needed (e.g., "Obtain Release of Lien" or "Request Endorsement") |

| Responsible Party | Who is responsible (e.g., Seller, Title Agent, Buyer’s Attorney) |

| Deadline | When the item must be cleared to avoid delays |

Assign specific roles to your team members: the title agent handles research and escrow, the underwriter assesses risks, and the attorney drafts any objections [2]. With clear roles and a solid tracking system, you’ll be ready to act quickly and efficiently when the title commitment arrives.

sbb-itb-df8a938

How to Read a Title Commitment (Texas) – Schedule A, B & C Explained

Schedule A Review Checklist

Schedule A is the first page of the title commitment, laying out the fundamental details of the deal before diving into exceptions and requirements. As Samuel B. Burke, Shareholder at Alagood Cartwright Burke PC, explains:

"Schedule A sets out the basic facts about the insurance contract, including the date the title commitment was issued, the name of the buyer and lender (if a lender is involved), the type of interest being conveyed, the amount of coverage the policy will provide, and a legal description of the property that will be insured." [3]

This section acts as a foundational review. Any errors here could derail the closing process, so accuracy is critical.

Verify Policy Information

Start by confirming the effective date. This ensures the title search is current. In Texas, title commitments generally arrive within 5 to 10 business days of opening escrow [2]. If the effective date is outdated, recent liens or property transfers might not be reflected.

Next, check the policy amount. For an owner’s policy, this should match the purchase price. For a lender’s policy, it should align with the loan amount [3]. Even minor mismatches can create coverage gaps. Also, ensure the insured names are consistent with the PSA (Purchase and Sale Agreement) and loan documents [3].

"Although this information is straightforward, it needs to be reviewed for spelling and other grammatical errors and to confirm that the amount of coverage is equal to the purchase price or amount of money being lent." – Samuel B. Burke, Shareholder, Alagood Cartwright Burke PC [3]

If the title commitment includes an arbitration provision, request its removal in writing before closing. This preserves the ability to take legal action against the title company in court if disputes arise [3].

Confirm Estate and Interest Type

Item 2 of Schedule A specifies the legal interest being insured. For a standard commercial purchase, this should state "Fee Simple." If the transaction involves a ground lease, it must state "Leasehold." Using the wrong term could result in incorrect title protection [2][3].

For deals involving a partial ownership stake, Schedule A must detail the exact undivided interest percentage being conveyed, not the entire estate. Double-check this against the granting clause in the PSA to avoid inconsistencies. Any mismatch between the PSA and Schedule A should be resolved before closing [2].

Validate Legal Description and Ownership

The legal description in Schedule A outlines the property being insured. Compare it word-for-word with the PSA, the ALTA/NSPS Land Survey, and any prior title records [2][3]. Pay close attention to boundary details, acreage, and lot or block designations. Even small errors, like a missing course in a metes-and-bounds description, can compromise the policy’s coverage.

Lastly, verify that the seller listed in the commitment is the actual record owner of the property [2]. In commercial transactions, especially those involving recent acquisitions, entity changes, or inherited assets, the record owner might differ from the contract seller. If there’s a gap in ownership, the title company must trace the title chain before moving forward.

Once Schedule A is thoroughly reviewed, proceed to the Schedule B Exceptions Review Checklist.

Schedule B Exceptions Review Checklist

Navigating the Schedule B exceptions review is a crucial step in ensuring a secure transaction. In Texas, Schedule B outlines the title risks that persist even after closing. As Impact Realty Group explains:

"Schedule B defines the risks that survive closing. If an exception stays, unresolved exceptions become part of your risk." [8]

This section highlights what the title policy excludes, and in commercial real estate, these exclusions can impact financing, construction, and long-term property value.

General vs. Specific Exceptions

Schedule B exceptions fall into two categories. General exceptions are standard and appear in nearly all Texas title commitments. These include items like unpaid taxes, rights of parties in possession (e.g., tenants), and "matters an accurate survey would reveal" [8][9]. While broad, many general exceptions can be narrowed or removed with the right documentation.

Specific exceptions, on the other hand, are property-specific and stem from the public records search. Common examples in Texas commercial real estate include utility and drainage easements, mineral reservations, Covenants, Conditions, and Restrictions (CC&Rs), and physical encroachments [8][9]. These exceptions can pose challenges, especially for development-heavy projects.

| Exception Type | Typical Impact on Commercial Real Estate |

|---|---|

| Utility Easements (10–30 ft wide) | Limits permanent structures and requires maintenance access [2] |

| Mineral Reservations | Potential surface disruptions; lenders may require waivers or endorsements [2][9] |

| CC&Rs | Restricts signage, business types, density, or architectural standards [2] |

| Encroachments | Could require resolving boundary disputes or removing structures before closing [1] |

Understanding these categories is the first step in addressing potential issues.

Review Referenced Underlying Documents

The title commitment provides a summary of exceptions, referencing recorded documents by Book and Page or Instrument Number. To fully assess the impact, you’ll need to retrieve and review these documents. Overlay easements and setbacks onto the current ALTA/NSPS survey to evaluate their effect [10]. For CC&Rs, check for restrictions that might conflict with your plans, such as limits on business types, signage, or density [1]. This detailed review helps confirm whether your proposed development is feasible.

"The list of special exceptions will contain the recording information for each item (the ‘Book’ and ‘Page’ where the document the exclusion refers to is filed in the county records) and a general description of each item." – Beth Ross, J.D., Nolo [10]

Options for Removing or Modifying Exceptions

Once you’ve identified exceptions, the next step is to explore remedies. Texas purchase contracts include a title objection period, typically lasting 5 to 20 days, during which you can formally challenge exceptions [2]. If exceptions remain unresolved, they become accepted by default, which can delay or even derail closing. Use this window to submit written objections for unacceptable exceptions. If no resolution is possible, the buyer may have grounds to terminate the contract [10][2].

For general exceptions, remedies often involve providing a seller’s affidavit to address "parties in possession" or obtaining an updated ALTA/NSPS survey to narrow or remove survey exceptions [11][10]. For specific exceptions that cannot be deleted, endorsements are a key tool. In Texas, endorsements such as the Access Endorsement (ensuring legal access to public roads), Contiguity Endorsement (for multi-parcel properties), and Restrictions/Encroachments Endorsement provide insurance coverage for financial losses tied to these exceptions [2]. While endorsements don’t resolve the underlying issue, they offer a layer of protection after closing.

Schedule C Requirements Review Checklist

Schedule C presents the final checklist of mandatory conditions that must be met before closing. Unlike Schedule B, which identifies exceptions, Schedule C focuses on resolving specific issues to ensure the title is insurable.

"The title company is essentially saying: ‘We’ll insure this title, but only after these issues are resolved.’" – Skyline Title Support [5]

Every Schedule C requirement must be addressed. Without meeting these conditions, the transaction cannot proceed to closing.

Standard Closing Requirements

Schedule C often includes essential tasks like recording the warranty deed, creating a new deed of trust for financed transactions, and releasing existing mortgages. For commercial entities – such as LLCs, corporations, or partnerships – the title company typically requires documents like certificates of good standing, franchise tax clearances from the Texas Comptroller, and corporate resolutions authorizing the transaction [5][12].

In Texas, community property laws may also require the seller’s spouse to sign certain closing documents. Identifying the seller’s marital status early can help avoid any last-minute complications at the closing table [5].

Tax, Lien, and Survey Issues

Unpaid property taxes are a common issue and are usually settled directly from the seller’s proceeds during closing. Another potential hurdle is "zombie liens", which are debts paid off long ago but never officially released. Sellers must provide a recorded release to resolve these [5].

If the property has undergone recent construction, sellers should submit an affidavit confirming full payment to contractors and subcontractors. This helps protect against unrecorded liens [1][5]. Survey-related problems, like encroachments or boundary disputes, are resolved through boundary line agreements, price adjustments, or a T-19.1 endorsement [5][2].

| Issue Type | Resolution Strategy |

|---|---|

| Unpaid Property Taxes | Paid at closing from seller’s proceeds; obtain recorded release |

| Mechanic’s/Materialman’s Liens | Affidavit of full payment and recorded lien release from contractors |

| Judgment Liens | Formal release recorded with the County Clerk |

| Survey Encroachments | Boundary line agreement or T-19.1 endorsement |

| Missing Heirs/Incomplete Probate | Affidavits of Heirship or court determination of heirship |

| Corporate Authority | Certificates of Good Standing and a Secretary’s Certificate |

Tracking and Clearing Schedule C Items

Resolving Schedule C items promptly is key to a smooth closing process. Once you receive the title commitment, treat Schedule C as a working checklist. Assign each item to a responsible party, set deadlines, and track progress [13].

"Treat Requirements as your closing checklist. Treat Exceptions as risks that will remain unless you address them." – Anna Morrison Lee, Broker [13]

For straightforward transactions, begin the title search at least 30 days before closing. For more complex commercial deals, allow 45–60 days to handle curative tasks like heirship filings or resolving zombie liens [5][13]. Always request an updated title commitment 24–48 hours before closing to confirm all Schedule C conditions have been met [2][5]. Double-check every item to ensure nothing is missed.

Risk Prioritization and Curative Strategies

After conducting detailed schedule reviews, the next step in the title review process is figuring out how to address the risks you’ve uncovered. Not all title issues carry the same weight, so understanding their severity and impact is crucial for deciding how to proceed.

Title problems can range from minor inconveniences to deal-breakers. The challenge lies in determining which issues could jeopardize the deal, which need resolution before closing, and which can be negotiated or accepted as-is.

Classify Title Issues by Severity

Title issues can be grouped into four tiers based on their seriousness:

- Deal-Killers: These are the most severe problems, like forged deeds, unresolved ownership disputes, or lack of legal access to public roads. Such issues can either end the deal or require costly legal fixes. For example, in early 2025, a Dallas investor nearly lost a $12 million mixed-use development deal due to a forged signature on a 1947 deed. Fixing it took eight weeks, expert affidavits, and a quiet title action costing about $40,000 [5].

- High-Priority Items: These include monetary liens, unpaid judgments, or unreleased lender documents. They must be resolved before closing.

- Negotiable Items: Issues like mineral rights, utility easements, or CC&Rs (Covenants, Conditions, and Restrictions) fall here. While they stay with the property, they can often be addressed through endorsements or price adjustments.

- Low-Impact Administrative Issues: These are minor problems, such as typos in legal descriptions or Schedule D disclosures, that are easily corrected with a simple affidavit.

"In Texas, mineral rights are the dominant estate: meaning the mineral owner’s rights typically override the surface owner’s rights." – Skyline Title Support [5]

| Severity | Category | Typical Issues | Resolution Strategy |

|---|---|---|---|

| Critical | Deal-Killers | Forgery, no legal access, unresolvable heirship | Terminate or pursue Quiet Title action |

| High | Schedule C Requirements | Tax liens, mechanic’s liens, unreleased deeds of trust | Payoff at closing; obtain recorded releases |

| Medium | Schedule B Exceptions | Mineral rights, major easements, CC&Rs | Endorsements (e.g., T-19.1); price negotiation |

| Low | Administrative | Typos in legal description, Schedule D disclosures | Corrective affidavits; simple document updates |

This classification helps guide the timing and approach for resolving title issues.

Match Curative Actions to Closing Timelines

Once risks are categorized, align curative actions with your closing schedule. Tight objection timelines demand swift action, especially for critical risks like legal access. Without recorded access, property values can plummet, and lenders may refuse to finance the deal [2].

To address these issues, use a formal objection letter within the objection window to notify the seller. This preserves your right to terminate the deal or compels the seller to resolve the issue, provide an endorsement, or negotiate a price reduction. Straightforward problems, like lien releases, are often resolved within a standard 30-day closing period. However, more complex issues, such as boundary disputes or missing heirs, may take 45–60 days. Legal actions like quiet title suits can extend to 12–18 months [5].

Common Curative Documents in Texas

The type of document required depends on the specific title defect. Here are some commonly used ones:

- Affidavits of Heirship: These address gaps in ownership when someone in the chain of title dies without a will.

- Correction Instruments: Used to fix clerical errors, such as misspelled names or incorrect legal descriptions in recorded documents.

- Releases of Lien: These confirm that a debt has been fully paid and clear it from the title record [4].

For transactions involving entities, an Authority Affidavit (as per Texas Property Code Section 12.019) confirms that the signer has the authority to act on behalf of the entity [4]. When removing an exception isn’t feasible, endorsements like the T-19.1 can shift the risk to the title underwriter, which is especially useful for survey issues or mineral rights complications [5].

"A purchaser is bound by every recital, reference and reservation contained in or fairly disclosed by any instrument which forms an essential link in the chain of title." – David J. Willis, Attorney, Lone Star Land Law [4]

Conclusion: Closing with Confidence

Texas title commitments serve as a detailed legal guide, outlining potential risks, obligations, and encumbrances tied to a commercial property. In Texas, this guide often traces back over 150 years, sometimes to original Spanish or Republic of Texas land grants [5]. Conducting a thorough final review ensures you can move forward with complete confidence in the integrity of your title.

Key Takeaways

To ensure a smooth closing process, here are the essential principles to keep in mind:

- Start early and act quickly. Addressing issues like zombie liens, heirship gaps, or errors in legal descriptions requires both time and precision [2][5].

- Schedule C is critical. Every item listed here must be resolved before the title company will issue insurance for the transaction [1].

- Understand Schedule B exceptions. These exceptions stay with the property, so cross-check them against a current ALTA/NSPS survey to confirm they won’t interfere with your intended plans [2][5].

- Act within the objection window. Texas contracts typically provide only 5 to 20 days to raise concerns about the title. Missing this window could mean losing the chance to request corrections [2].

- Verify an updated title commitment before closing. This ensures all Schedule C requirements have been addressed.

"Studying the Texas title commitment early protects value and guides negotiation." – LandQuire Team [2]

How The Fractional Analyst Can Help

Title review is a crucial step in commercial real estate transactions. The Fractional Analyst simplifies this process by integrating title-related data – such as easement impacts, lien payoff amounts, and Schedule C requirements – into financial models. Their CoreCast platform and expert team provide actionable insights and tools for accurate underwriting and risk evaluation, ensuring you’re well-prepared for closing.

FAQs

What’s the difference between Schedule B exceptions and Schedule C requirements?

Schedule B highlights items that the title insurer won’t cover unless specifically removed or addressed with an endorsement. These can include things like easements, mineral rights, or recorded restrictions. On the other hand, Schedule C focuses on issues that need to be resolved before closing, such as probate or tax problems, to ensure the title is clear. Simply put, Schedule B deals with ongoing limitations, while Schedule C outlines conditions that must be met before the final title policy is issued.

What Texas title issues can derail a CRE closing?

In Texas, a commercial real estate (CRE) closing can face serious delays or even come to a halt due to title-related problems. Some of the most common hurdles include unresolved title defects, exclusions, or exceptions listed in the title commitment. If these issues can’t be resolved or waived, they can prevent the issuance of a clear title policy. Without a clear title, the transaction simply can’t move forward.

What endorsements should I ask for in a Texas CRE title policy?

In a Texas commercial real estate title policy, it’s important to request endorsements that tackle crucial title concerns and expand your coverage. Some commonly sought endorsements include those covering restrictive covenants, water rights, ad valorem taxes, and subordinate liens.

Pay close attention to the Schedule B exceptions. Carefully review these exceptions and request endorsements to either remove or clarify them. This step ensures you have stronger protection for the property and reduces potential risks tied to unclear or unresolved title issues.

Leave a Reply